Donald Trump has declared Healthcare is Complicated. Who knew? As the Affordable Care Act (ACA) continues to crumble and Republicans can’t agree on a coherent replacement, a crisis of some sort is in the offing. This is what happens when you ignore health care’s relationship to personal finance and the basic principles of insurance. Suddenly, we are all aware pre-existing conditions is a huge stumbling block. It’s the reef wrecking all the offered solutions. The ACA’s solution was to try to force healthy young people to greatly overpay for health insurance in order to bail out insurance companies forced to insure sinking ships. This violates every principle of insurance. No wonder the ACA in a death spiral. You’d think the Republicans after eight years would’ve come up with something better, but not these geniuses. When you have a problem, solve the it without making new and potentially bigger problems. Face up to pre-existing conditions.

Dave’s Plan (series under Dave’s plan to fix the ACA starting in 2014) is the only plan biting the bullet and ultimately eliminating the problem. First of all, covering pre-existing conditions costs money, lots of it. Expecting young people just starting out in their careers and raising families to pay for older sick people along with their student loans is let’s face it is insane. The only reason anyone would propose such a noxious solution is the political fact young people don’t vote in the numbers as older people. They forgot people also vote with their dollars and healthy young people didn’t sign up to be screwed under the ACA. Now the political class on both side of the aisle are faced with increasing the penalties on the young if they don’t buy overpriced policies and risking a revolt of the young bringing into question not only the ACA but Social Security and Medicare. They’re burdened with paying for these but they may not be there when they get old. Millennials are the largest group in our population. Do politicians really want to piss them off and politicize the young? Better to face the problem up front and pay for it directly and eliminate it in the future.

The Personal Benefits Account (PBA) proposed under Dave’s Plan requires the first $10,000 in the account adjusted for inflation be invested in a Government liquid fund. This would allow for the Medical Credit Card payments the to cover deductible before the Catastrophic Insurance kicks in. In any case, investment accounts always need a cash buffer so investments aren’t liquidated at an inopportune time to meet a current expenses. Lower income people surely shouldn’t put their first savings dollars at risk. This common sense provision would create in a great money pool in the Government Liquid Fund. According to the American Benefits Council as of April 2014 there were 73,668,000 active participants in 401k type plans with the vast majority having assets greater than $10,000. Under Dave’s Plan number would more than double. As the late great Senator from Illinois Everett Dirksen was attributed as saying, “A billion here, a billion there, and pretty soon you’re talking real money.” We’re talking real money here. As this would be a higher yielding fund(3%, balances adjusted for Inflation at medicare age) we need to get the best ultimate return for the nation. This spoonful of sugar to make savings more palatable is going to cost more. Fully subsidizing high risks pools for pre-existing conditions and providing overdraft protection for the associated credit cards would provide this return.. Remember, all the catastrophic plans in the PBAs would be owned by individuals therefore portable, non-cancelable and with no lifetime limits (yes you can stay on your parents plan till 26). These policies would still be relatively inexpensive since they initially would be insuring only healthy people, have no payment problems and sold on a national basis . This allows insurance to adhere to real insurance principles. Under this plan the pre-existing condition problem would ultimately simply cease to exist. As older sicker people move on to medicare or sadly die, it would disappear. As those with per-existing are heavily concentrated in the 50 to 65 age group, most of the problem would be gone in 15 years. The cost ends rather than going on into eternity. In the long run a huge savings. We’d be left with a population insured at a reasonable price. Not a bad investment. Nobody seems to agree how big the pre-existing condition universe is. We’ve heard everything from 500,000 under the ACA to 133 million. For our purposes they would be those who wouldn’t be offered a catastrophic policy with a deducible easily handled the PBAs $10,000 portion. Whatever its size, the end of the problem would be in sight.

Even of greater importance to the future cost of medical care is the overdraft protection for the PBA’s associated credit card. Given the fact the PBA would have a constant cash flow either from the minimum 10% of income, subsidy, Medicaid or a combination, this doesn’t require any large amount of money. Just smoothing things out. What is important is that providers have no credit risk. What we need is the vast majority of medical transactions be done on a cash or credit basis. No third-party involvement, except for the small minority of transactions paid by catastrophic insurance. Why is this so important? It is the only way to deliver quality health care without rationing and/or price-fixing. Bob Blayter, who writes the monthly “Stretch Your Dollar” column in the Arizona Republic provides us with this personal insight:

I discovered that when I tell doctor’s offices , labs, or imaging centers that I’m a cash patient they extend generous discounts. For example I was told the cost of a CAT scan was $1500, but when I told them I was a cash patient the charge dropped to $399. They even offered to take payments with no interest.

Or consider Melinda Beck writing of Direct Primary Care Practice in the Wall Street Journal:

There’s’ no waiting room at Linnea Meyer’s tiny primary care practice in downtown Boston. That’s because there’s rarely a wait to see her. She has only 50 patients to date and often interacts with them by text, phone or email. There’s no office staff because Dr. Meyer doesn’t charge for visits or file insurance claims.

Patients pay her a monthly fee—$25 to $125, depending on age—which covers all the primary care they need.“Getting that third-party payer out of the room frees me up to focus on patient care,” says Dr. Meyer, who hopes to expand her year-old practice to 200 patients and is relying on savings until then. “This kind of practice is why I went into medicine, and that feels so good.”Dr. Meyer is part of a small but growing cadre of doctors practicing “direct primary care,” which bypasses insurance and charges patients a monthly membership fee that covers everything from office visits to basic lab tests. It’s similar to “concierge medicine” but less costly: The average monthly fee for direct primary care is $25 to $85, according to the Direct Primary Care Journal, a trade publication.

What do these examples point out? Third Party Pay is very expensive. Going to a mainly cash system would give us huge savings. Of course, we’ve known this for a long time. While the cost medical care has been going up in various multiples of the inflation rate, cosmetic surgery always done on a cash basis has barely budged in price. In 2015 the last figures available U.S. health care spending increased 5.8 percent to reach $3.2 trillion, or $9,990 per person. If we can just bend the cost curve down by just 5% we save $1.6 trillion over the next decade. 10% we save $3.2 trillion.

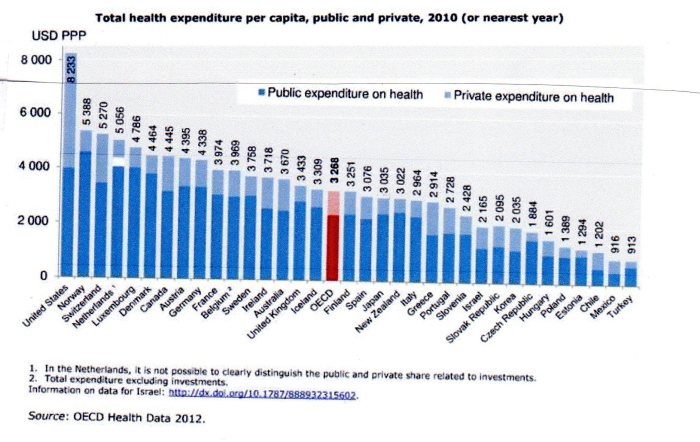

Greatly limiting third-party involvement isn’t the only way the credit card potentially saves a bundle. By creating a huge credit worthy market, a critical mass, we present providers and potential providers with an enormous target for competition and innovation. Does anybody think this won’t result in more savings? Is there room to actually dramatically increase savings in healthcare? Consider this OECD chart costs among its members:

We can see Americans pay 1 1/2 times the next most expensive country and 2 1/2 times the OECD average. If allowed, we believe American innovation and ingenuity along greatly reduced 3rd party pay and elimination of preexisting condition problem, can substantially narrow the gap.if not entirely eliminate it.

Some have questioned the interest cost on the liquid Government guaranteed portion of the PBA. Granted 3% adjusted for inflation at medicare age for inflation is generous compared to what the government pays for funds today. But we want to encourage our savers to save. However, this return isn’t out of line with historical norms. Compared with what the government paid in 1980 it’s a bargain. More important, 1/3 of Americans have no savings. Another 23% have less than $10,000. This plan virtually assure Americans have at least $10,000 in current buying power at retirement. Given the lifetime savings nature of the PBA most people will have a lot more than that. This is important because those retiring with just social security will need government support at probably every government level. Sort of pay now or pay a lot more later. If generosity now encourages people to save, it’ll save the government big bucks in the future. In fact, with us heading towards two workers supporting each retiree, increased savings maybe the only way out of a future disaster. A complete listing of the PBA’s benefits can be found in our post A Party Platform?

We had hoped by now to post a direct comparison of Dave’s Plan with the Republican ACA replacement but that bill seems to be in the witness protection program somewhere. If and when it surfaces we will post ASAP.