The Biden administration claims it can do little about inflation and leaves it up to the Federal Reserve (Fed) to tame prices. The Fed can bring inflation to heel if it will raise interest above the expected inflation rate. Anything less adds to costs while still encouraging borrowing. For instance, you’re buying a house with a 5% mortgage. It sounds high by recent standards, but if inflation is over 8%, the actual rate is -3 plus the interest tax deduction. This interest rate won’t deter people from buying houses or other capital goods. It just adds to demand and costs. Aso, don’t forget rising interest rates add 100s of billions to what we pay on our national debt, adding to rather than solving the problem.

However, if you drive up the interest rate above today’s 8-9% inflation, the economy probably will fall out of bed as it did in the early 1980s. People forget at the same time Fed. Chair Paul Volker was driving interest rates to 18%; we laid the groundwork for a rapid recovery.

The Carter Administration deregulated industries such as Airlines, Railroads, and Telecommunications. Pres. Reagan extended this trend by dumping gasoline price controls, among others. He also cut taxes where inflation had pushed people into ever higher brackets. These were all supply-side incentives and turned the early ’80s recession into the excellent expansion that continued through the ’90s.

It may be too late to avoid a recession, but we can try. Biden needs to emulate Carter and Reagan by expanding goods and services rather than maintaining his current roadblocks. The quicker we increase supply, the less the Fed will need to raise interest rates.

Energy is essential to everything we do; it’s the place to start. Once again, let me lay out the economics. I’ve said it before, the view our future production doesn’t affect world prices is bogus. Yet, the Washington Post economics writer Charlotte Rampell echoes others by saying our energy production doesn’t affect prices.

Experts estimate excess production in places such as Saudi Arabia and the Emirates at about 2-3 million barrels daily. This production is the oil Biden will try to talk the Saudis into pumping to bring down prices. The problem is there is no incentive to pump more. The Saudis may promise to pump a few more barrels for political reasons, but not enough to lower prices.

Those with oil in storage also have no reason to rush the product to market if they feel the price is rising. Instead, they might buy cheap Russian or Iranian oil and hold it for sale later. It’s hard to estimate the stored amount at any moment, but we know it adds to price pressure. Think of toilet paper during the pandemic. People hoarded it as long as it was dear.

The possibility of more oil coming to market changes everyone’s outlook. If we gave U.S. producers a clear playing field rather than threatening their existence, we could add millions of barrels daily to the market in the future. Further, rather than discouraging investment, we could use our expertise aboard to bring in even greater production worldwide.

Saudi Arabia, seeing competition and market loss in the future, would rather sell at today’s high prices, forestalling others from replacing them in the market. Others with shut capacity would join in pumping millions of barrels today.

Fearing a basement full of toilet paper with decreasing value, hoarders disgorge their stash. Likewise, those holding oil off the market will now sell. Even if hoarding only accounts for 3-4%, it means a 6-7% change. You’re selling and depressing prices instead of buying to add to the stockpile pushing up prices. We change the market when we add to prospective new supply.

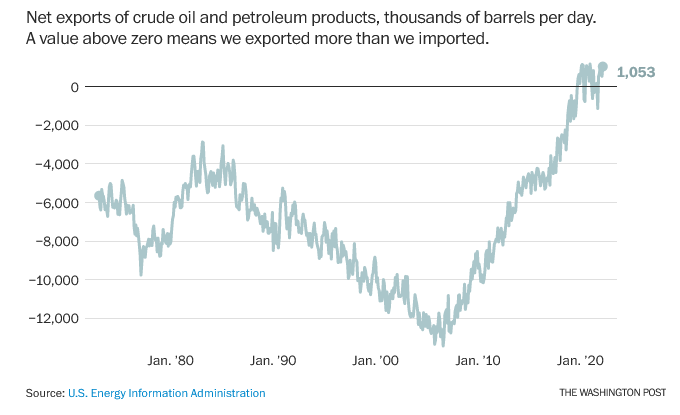

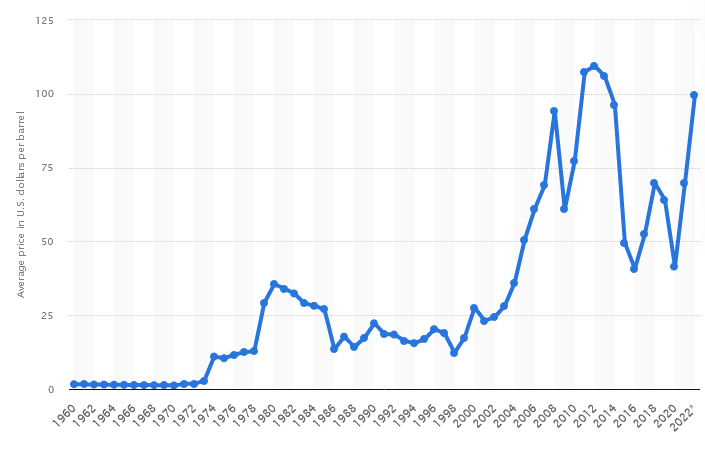

The margin is where we set prices. A swing of 5-15% can stop a rising market and start it in the opposite direction. Prospects affect actions today. That’s why we have futures markets. Rampell’s chart illustrates how this is true. So long as U.S. crude output was rising, we had low prices only interrupted by short-term disruptions:

The chart shows our production is now is well below trend and in fact, leveled off. In a world with an expanding thirst for oil, our failure to reach 15 million barrels daily contributes to the price rise. Conversely, pumping that much oil would be a check on prices. The price of oil seems to be the inverse of U.S. production:

The rationalization for opposing every energy source but wind and solar is spurious. The claim is this will cut carbon emissions and stall global warming. The reality is the world gets 80% of its energy from fossil fuels. The reason we use them is simple; they’re cheaper and more reliable than anything else.

Throughout history, humans have opted for more affordable energy. People will change fuel sources to cut carbon emissions if it doesn’t cost them more. They won’t if the costs lower their standard of living.

High-cost energy leaves plenty of room to be supplanted by innovation, stranding costly overpriced investment. We adopted beasts of burden because they were cheaper in terms of productivity than human power alone. We harnessed the wind and water for the same reason. Fossil fuels replaced all these because they were more affordable and reliable. We have never gone backward and returned to more expensive, less reliable energy.

Economist Stephen Moore makes a good argument in the Washington Examiner that the administration’s green policies will never work. It requires too much space and high carbon inputs.

Billions of people worldwide are still without reliable electricity. For those that do have electricity, 40% is coal-powered. The idea these people will opt for expensive, unreliable imported windmills and solar panels flys in the face of history.

There is no reason to believe there isn’t plenty of natural gas to replace current and future coal usage, cutting those emissions in half or more. You have to have reliable energy to back up when the sun doesn’t shine, or the wind doesn’t blow; why bother with wind or solar power except in particular circumstances?

The major problem with expanding natural gas use is political rather than availability. For example, the vast new gas field in the eastern Meditteranean is attracting European Union orders to replace Russian production, but there are obstacles. The one Egyptian liquid Natural Gas facility is near capacity. Building more takes significant capital investment, but the Europeans are reluctant to commit to long-term contracts in the face of extreme Green resistance. Of course, an undersea pipeline would be best, but according to the Wall Street Journal, the U.S. joined in opposition for environmental reasons.

Without the emerging world cutting their emission, nothing we do here, everyone driving a Tesla and solar panels on every roof, will make a difference. They need to grow their economies for their people to have better lives. Using fossil fuels until something cheaper and more reliable comes along is a necessity. Wouldn’t half a loaf with natural gas be better than coal, wood, or dried cow dung?

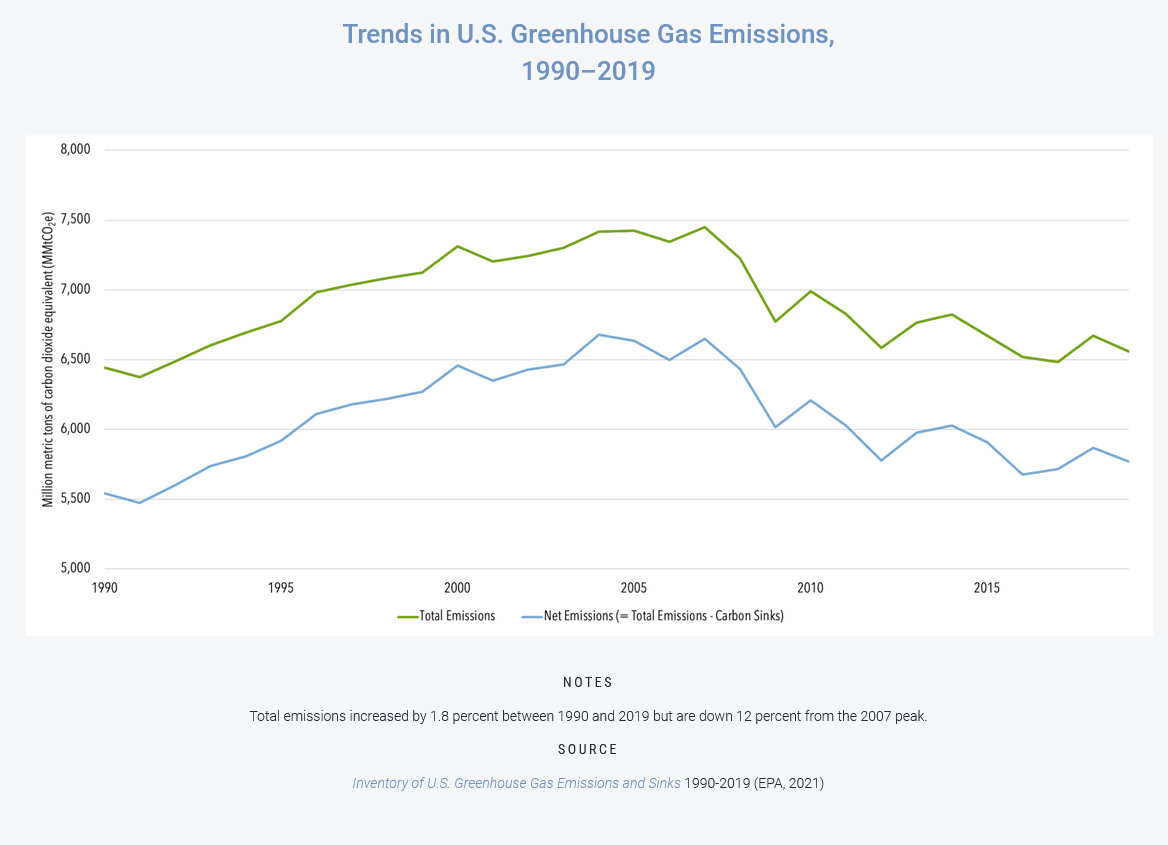

According to the Week magazine, the world just set another carbon emissions record, yet the U.S. has reduced emissions, so we aren’t contributing to the increase. Natural gas replacing coal is the primary reason:

We need to get back to basics. Upon taking office, Reagan dumped controls of gasoline. With profits incentive restored, everyone the world over was looking for oil. The price stopped going up. Over the next decade, it fell to $10 from over $30 a barrel. If the prospective supply of anything looks to increase in the future, it will exert downward pressure today.

Simple economics, but that’s something lost among our elite economic community. After all, 17 NobelPrise economists backed Biden’s Build Back Better massive spending to add to his other huge expenditures. If our inflation is terrible now, what if we followed their advice?

Some people need to go back and reread Adam Smith. The title, Economist, is becoming a dirty word. Smith himself was a moral philosopher (his first book was “the Theory of Moral Sentiments”). The term “Economics” came into use about 100 yrs after his “Wealth of Nations” was published.

In the next installment in this series on how to handle inflation, I’ll show how to apply the principles I’ve used for gas and oil across the economy to tame the inflationary beast. Maybe Biden has no idea what actions to take, but I do.