A great idea without the capital to make it happen remains just another missed opportunity. Tune in the TV show”Shark Tank” and you get a good idea of the important interplay between ideas and the where with-all to implement them. So what is this lubricant to ease us into a better future? Capital is deferred consumption. Early on someone realized that eating all the grain they found left no seed to plant and surely none to increase the acreage under cultivation. To have more meant setting aside “seed corn”. Put off eating the sheep and you can get more sheep and warmth while you wait. If we have more grain, wool or meat than we can presently use we can trade it for other stuff. In a nutshell, we have “More”.

The problem arose when trades were inconvenient because of time, place or both. Entity A has fish to trade for wine, entity B has wine but doesn’t need fish at the moment. Entity C needs fish and has pretty rocks from which metal could be extracted to trade. Now A finds it could trade C’s pretty metal for B’s wine. More importantly, where wine and especially fish could spoil and were bulky to store, the shiny metal could be shaped for easy storage or trade and it never spoiled. With these attributes it performed a further function, a store of value.

The wide-ranging trade of the Phoenicians from the Red Sea to Great Britain was greased with Spanish silver. Without it, it’s hard to see how this trade could flourish by simple barter. While some people used beads or shells, people from China to Britain accepted of gold and silver coin and bullion, thus making multi sided trading a reality with trade in China and the Indian Ocean following a similar path as the Phoenicians. The effect of this for civilization cannot be over estimated. The needs of trade and capital spread what we call the 3 Rs far and wide.

With an established store of value, lending and investment could fuel the attainment of “More”. Without a great investment of capital, British Tin would never have made it to Egypt or finished goods from everywhere in Britain. Without capital, trade could never have expanded across so much of the world.

Why did people forgo consumption to use their accumulated store of value to build ships to sail far and wide? Surely they knew the ship could sink in a storm or on a reef and all would be lost. Why take the risk ? Simply for the potential reward. Bringing back wonderful goods when successful far surpassed occasional loss.Without a favorable risk reward situation no ship would ever leave port. If you want the economic betterment ship to leave port, a political entity would find it in their interest not to add to that risk or reduce the potential reward. History shows political entities that respected and protected people’s capital thrived. Those that steal or tax (some might say they’re the same) away people’s foregone consumption (capital) to fund the controlling elites and those they favor find it tends to leave. For instance, in Europe from 15th century Venice and Florence to modern-day London the greatest prosperity appears where capital is treated fairly.

Russian money fuels markets in London. Chinese money flees to Vancouver and South Korea’s Jeju Islands and Latin American money flows into Miami. Fear that the governing elites will grab their stuff or worse moves people to preserve what they have in a safer place. The countries that already have grabbed peoples stuff such as Cuba or Venezuela , well they have virtually no capital.

While historically the US has been welcoming place for capital, there are troubling trends. Corporations earning profits all over the world are parking them overseas to avoid punitive taxes. Worse corporations are leaving our shores to join their money.(Inversions). This is visible for public corporations but we have no idea of how much private money and businesses have left. Judging by the moves of public companies this will also prove to be substantial. Adding to our potential woes, our leading candidates for President are anti-trade and might pull out of our present trade agreements and rule out future ones. What a stop sign to investment capital. A foreign chemical company might want expand in the US because of our great comparative advantage in natural gas feed stock but being locked out of the world market would rule it out. Threats from the present administration and those that will lead in the future to businesses that need to make sensible moves is a big signal to other businesses foreign and domestic to go somewhere else. Ford Motor is opening a small car plant in Mexico in part to take advantage of lower labor costs on very low profit margin cars. Americans don’t really buy really small cars, but they can be sold on the world market. Mexico actually has better trade arrangements with the rest of the world, so building and selling from Mexico makes perfect sense. The leading candidates however show no love for Ford, and in fact one would hammer the company with tariffs and more. This is hardly an invitation to both foreign and domestic companies to expand in the US. Tow our government line or else, isn’t fun for Ford, but an insult to BMW or Toyota or anyone else that might expand in our country. How any of this attracts capital to make and service stuff and put people to work is a mystery. We must never forget the close correlation friendliness to capital to prosperity.

Throughout history no entity was made poorer by having too many rich people. Conversely, rich people leaving leads to distress. For instance, if it wasn’t so tragic, the fact that New Jersey faces a dire budget shortfall because one person, hedge fund manager David Teppper, is leaving the state for Florida sounds like a comedy routine on how not to treat capital and those that possess it. Taxes, over regulation and favoritism by governments can indeed hang out a capital not welcome sign. The average person may not see it but people with capital can surely can and adjust accordingly.

Not all actions that distort natural capital flows come from politicians or rulers inclined to grab somebody’s wealth to benefit themselves and their own supporters. Sometimes distortions arise for the best of reason. Most regulations are based on some perceived need to better people’s lives. Where they go off the rails is when they aren’t subjected to cost benefit analysis before and after implementation.This would prevent expensive overkill or a diversion of resources to the favored. What everyone needs to remember is that those who possess capital live with us and want where they live to be better. Throughout history the wealthy have contributed to the livability and betterment of their communities. Look around and see that park, museum or school. Who are the big benefactors of our charities? As we have said communities are better off with more capital not less. Generally all it wants is to treated with fairness and justice. The fact this isn’t so common in this world is why it changes often changes neighborhoods.

No one would say the people who run the world’s major central banks are bad people. Quite the contrary, leading bankers and economic scholars, they represent an elite charged with maintaining the prosperity of the people they serve. Our Feral Reserve is besides being the bank’s bank for stability of the system is charged with both maintaining price stability and full employment. These wise elites have pursued these often contradictory goals with increasing fervor with questionable success. What could be purchased for $100 at Fed’s inception in 1913 would take $2,416.78 or a cumulative rate of inflation of 2316.8%. So much for its effect on price stability. As for full employment, one can’t be faulted for lack of effort. Since the 2007 recession, the Fed along with other major central banks have kept interest rates near zero if not negative to spur employment. Even with enormous purchases of bonds to maintain artificially low-interest rates, the economies they serve have experienced the slowest growth ever recorded coming out of a recession and this for 8 years. But it has resulted in infusing the entire world economy with possibility of terrible risk.

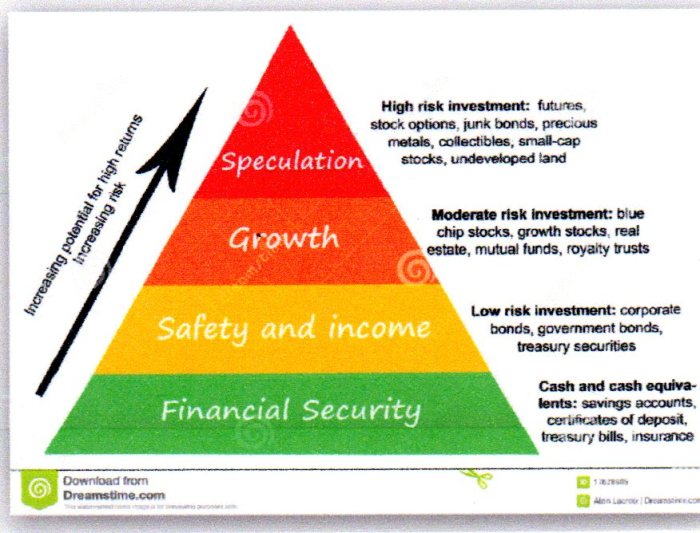

So why are the World Banks effort failing to provide the desired results? It could be these bright people are operating under a faulty theory. The idea behind zero or less interest rates is by taking away the safe returns of top quality bonds, it would force money into risky but job producing investments such as new innovative businesses. On the surface this seems to make sense but in the real world could be producing the opposite effect.The idea is Investors will move their assets directly from low to high risk is at the heart of the theory. In the real world individual or institutional investors think in terms of asset allocation. If you’re a fiduciary such as a trust, pension fund or insurance company that control huge pools of capital , you have to act as a “prudent person”. You might have to regularly disburse funds while preserving buying power for the future. Normally, an investment allocation pyramid would look something like this:

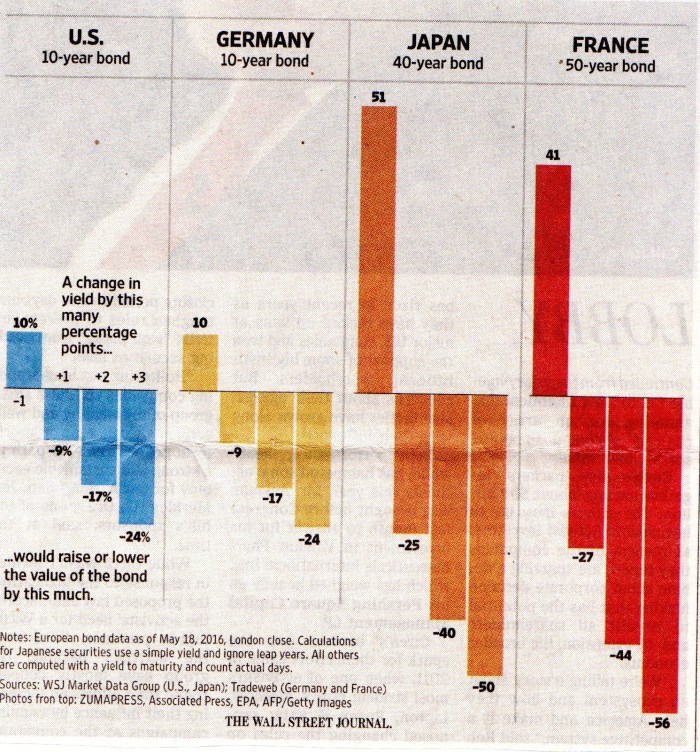

In this standard allocation, the base two categories to provide for any present cash needs while the top two maintains or hopefully increases future purchasing power. Not having to sell assets in a down market to pay for present needs avoids destroying principle and this what “prudent people” do. Allocating the actual amount in each category would mirror actual individual or institutional needs. The bottom two categories are fixed income and directly respond to the central banks setting interest rates. Under the central banks present policies these have changed from stable and safe to volatile and risky without any corresponding increase in fixed return. Just how inappropriate these have become is apparent by this chart of how Government bond values would respond to even small changes in interest:

Only by rates moving even deeper into negative territory can bonds show any increase in value. However, the more likely increase in rates would have a devastating on the value of the bonds. While the bonds could conceivably be held to maturity with no loss of principle, US 10 yr Notes yield 1.85%. This is lower than the Feds stated inflation goal of 2 %. Risk for no real return. At 2.54% the Us 30 yr Bond presently gives a slight positive return, but at a horrible risk to principle. For the prudent investor this removes the solid base of the pyramid. We are then left with only the top two, risk and high risk, as possibilities. Well, isn’t this what the central banks wanted? Yes,but the portfolio now has way too much risk to be prudent. Any business downturn with its accompanying stock and real estate market declines would jeopardize principle if cash is needed to pay current obligations in a down or illiquid market. This would argue for concentrating on dividend bearing stocks or income properties.These are overwhelmingly mature companies and existing properties located in the third tier. New businesses and building use cash not throw it off so investment would in fact move away from the top high risk tier to reduce imprudent risk and gain necessary income. To the extent the investor feels the need for cash reserves to cover out of the ordinary experience and/or to take advantage of better investment opportunities, funds are further diverted away from the high risk top-tier to the bottom no income tier.

How can we tell if The Fed is correct or counter productive? We would’ve seen a surge in new business formations resulting in greater competition for existing businesses if money was in fact moving into the top tier. In fact the opposite has happened. New business formations have declined during the entire period. Existing businesses rather than having profits pressured by new hungry competitor’s, have according to The Economist’s March 26th issue headline “Too Much of a Good Thing. Profits are too high. America needs a giant dose of competition”. The existing companies in the S & P Index are selling at near record valuations. Capital is flowing opposite from the Fed’s projection. Why not? Established Companies have credit ratings that give them access to the low rates that the Central banks have dictated. New and small business have a much more difficult time with credit and other regulations. All this increases risk and lowers their investment attraction.

We all can see this on a personal level. The Banks of Mom & Dad or Grandma and Grandpa are likely to be constricted or closed. Worried about the higher risk they are living with, they’re just not open to more. Yet friends and family often were the sources of seed capital for new businesses. We know from our own experience, fiduciaries are too worried about risk in the investments they have to think about adding more.

We aren’t the only ones feeling the risk. Martin Feldstein,chairman of the Council of economic Advisors under President Reagan, writing in the Wall Street Journal 5/17/16 put it this way

…interest rates remain excessively low and are still driving investors and lenders to take unsound risks to reach for yield, leading to a serious mispricing of assets. The S & P price-earnings ratio is more than 50% above its historic average. Commercial real estate is priced as if low bond yields will last forever. Banks and other lenders are lending to lower quality borrowers and making loans with few conditions.

When interest rates return to normal there will be substantial losses to investors, lenders and borrowers. The adverse impact on the overall economy could be very serious.

So here we have we have good highly intelligent people for the best of reasons pursing policies that not only fail to achieve their goals, but actually might end in bad unintended consequences. Some are beginning to question the basis of these “wise people” having this kind of power. Former Bank of England Governor Mervyn King in his new book “The End of Alchemy: Money, Banking and the Future of the Global Economy” puts it this way

I came to believe that fundamental changes are needed in the way we think about macroeconomics, as well as the way central banks manage their economies. A key role of a market economy is to link the present and the future, and to coordinate decisions about spending and production not only today but tomorrow and in the years thereafter. Families will save if the interest rate is high enough to overcome their natural impatience to spend today rather than tomorrow. Companies will

invest in productive capital if the prospective rate of return exceeds the cost of attracting finance. And economic growth requires saving and investment to add to the stock of productive capital and so increase the potential output of the economy in the future. In a healthy growing economy all three rates—the interest rate on saving, the rate of return on investment, and the rate of growth—are well above zero. Today, however, we are stuck with extraordinarily low interest rates, which discourage saving— the source of future demand—and, if maintained indefinitely, will pull down rates of return on investment, diverting resources into unprofitable projects. Both effects will drag down future growth rates. We are already some way down that road.

With capital flows are so integral to our journey to “More” maybe they are too important to be left to modern Alchemists no matter how well-meaning. Limiting Central Banks to being the Bankers Bank to prevent panics and the so far failed task of maintaining purchasing power is a full enough plate and they need to be relieved of this quest for ” Full Employment”. In any case that never made sense in anything but a political way. The unemployment rate is merely a coincident indicator, meaning other things have to happen before it improves. Making the actual circumstances for improvement in growth easier would prove more beneficial. It is definitely time to stop thinking in terms of top down elite leadership and thinking of leaving things to bottom up natural solutions I.E. It brings to mind Matt Ridley in his recent book ” The Evolution of Everything: How New Ideas Emerge”when he noted

To put my explanation in its boldest and most surprising form: bad news is man made, top–down, purposed stuff, imposed on history. Good news is accidental, unplanned, emergent stuff that gradually evolves. The things that go well are largely unintended; the things that go badly are largely intended.